[ad_1]

We know there’s been a lot of conversation surrounding the news about Silicon Valley Bank and, naturally, you may have questions. It’s important for you to know that your money is safe with SoFi. We have a high quality growing deposit base. We have ample cushion to the regulatory required equity to asset ratios. We have maintained a strong spread between what we charge on loans and our cost to fund loans despite a higher interest rate environment. 90% of our deposits are insured. Importantly, we have no assets with Silicon Valley Bank—our only exposure is a small lending facility (i.e. the ability to borrow money) under which we have borrowed less than $40m, and which is unaffected by the FDIC’s receivership of Silicon Valley Bank.

Trust and safety for our 5.2 million members and their money are our number one priority, which is why we want you to understand all the ways we work to keep your money safe. As a nationally chartered bank, SoFi is focused on complying with the strict regulatory standards it is held to by the Federal Reserve, the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation (FDIC), the Securities and Exchange Commission, the Securities Investor Protection Corporation, and others. Below we outline the capital ratios that we must meet or exceed as required by our National Bank Charter. In addition, SoFi Bank deposits are insured by the FDIC up to $250,000 per individual and $500,000 per joint account, and we can help protect your accounts from fraud with 24/7 account monitoring and the ability to freeze your debit or credit card instantly in the SoFi app.

We thought it was worth taking this opportunity to underscore some characteristics of our strategy and our business model, specifically as it regards our Checking and Savings products offered through SoFi Bank.

Our goal is to provide our members with best-in-class products that help them get their money right across convenience, speed, content, and cost. First, we provide a highly competitive interest rate on checking and savings. This key point of difference along with our fully digital capability to spend, save, and pay all from your phone helps drive people to use SoFi as their primary bank account, as evidenced by high-quality direct deposit growth. In fact, 88% of year-end 2022 deposit balances were from direct deposit members, and roughly 50% of newly funded SoFi Checking & Savings accounts are setting up direct deposit by day 30.

These strong trends have not changed, as we surpassed $7.3 billion in deposits (up 46% quarter-over-quarter) in Q4’22. Our average balance for direct deposit members is just under $25,000, which is FDIC-insured. In fact, over 90% of our deposits are insured, which is well above industry benchmarks.

The effective spread we earn between the yield on our loans and the interest paid to our members on their deposits (as well as other sources of capital) enables SoFi to continue to innovate and invest in product differentiation, better services, better prices and more competitive rates for our current and prospective members.

We know trust and the safety of your money are top priorities when selecting a bank, and we take that very seriously here at SoFi. Helping you achieve your financial goals and feel good about your money, while doing it is our number one priority.

We’ve included answers to some FAQs we’ve received from investors and shareholders below.

Frequently Asked Questions from Investors & Shareholders

Do you have exposure to Silicon Valley Bank (SVB)?

We do not hold assets with SVB. Our only exposure is a small lending facility under which we have borrowed less than $40m and which is unaffected by the FDIC’s receivership of SVB.

Are my deposits insured and to what amount?

SoFi Bank deposits are insured by the FDIC up to $250,000 per individual and $500,000 per joint account.

How many deposits does SoFi have? How many of those are above the FDIC insurance limits?

As of the end of Q4’22, we had $7.3B in total deposits, up $2.3 billion versus Q3’22. We see strong growth continuing in 2023.

We have not historically provided information on the average deposit balance at SoFi, nor the number of accounts funded above the FDIC threshold of $250,000. However, we provided in our recently-released annual report on Form 10-K that as of December 31, 2022, the amount of uninsured deposits totaled $615.9 million, meaning over 90% of our deposits are insured.

How do you think about the stickiness of your deposits versus people just chasing the best rates?

As of the end of Q4’22, 88% of our member deposits were from direct deposit accounts. Direct deposit helps drive people to use SoFi as their primary bank account. This view is also consistent with federal banking regulations that recognize the stickiness of retail deposits.

What other sources of funding do you use for loans to SoFi members? Is there a limit or ratio of how much of the deposits you can use?

We rely upon deposits, warehouse line financing from large money center banks and our own capital to fund loans to members. As of year-end 2022, we had borrowing capacity of $8.4bn under loan warehouse facilities, of which $3.1bn, or 36%, were drawn. Additionally, we have approximately $3 billion in our own equity capital that we can use to fund loans and, as mentioned above, $7.3 billion of deposits at the end of 2022, and we see strong growth continuing in 2023. In total we have ~$18 billion of available capacity to fund loans and meet our liquidity needs.

What has been the trend in deposits?

Deposits grew by $2.3bn in Q4’22, by $2.3bn in Q3’22 and by $1.6bn in Q2’22.

Do you have a portfolio of AFS (available for sale) securities?

As of YE22, we have only $195mm in fair value of AFS debt securities of our total assets of $19 billion. These consist primarily of U.S. Treasuries (60%), with 48% of the securities due within one year, and 93% due between 2-5 years.

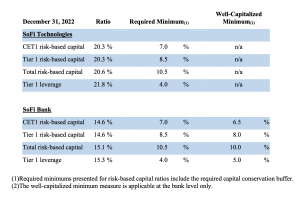

Are there limits to how much you can lend?

Yes, in addition to our judgment of sound business strategy and practices in order to drive shareholder value and the additional oversight of our risk committee, credit committee, and various Federal regulators, we are required to meet certain capital ratio minimums. Specifically, the table below outlines each capital ratio minimums required at our OCC Bank Charter and at our holding company, as well as our reported capital ratios, which exceed all requirements by significant amounts.

If there are loans on your balance sheet, how do you protect their value if the loan’s rate is fixed, while Fed Funds and benchmark interest rates increase?

When we fund a loan we hedge the interest rate risk of that loan in order to account for the risk to the value of the loan from interest rates changing. Specifically, we enter into derivative contracts to manage future loan sale execution risk for loans on our balance sheet. Our hedging intentions are to economically hedge the risk of unfavorable changes in the fair values of our personal loans, student loans and home loans. Our derivative instruments used to manage future loan sale execution risk include interest rate swaps, interest rate caps and home loan pipeline hedges.

Does the potential impact of the SVB receivership on start-ups affect your business?

We do not offer business banking services, so we do not take deposits from or make loans to businesses of any size, including start-ups. However, we do count among our Technology Platform customers several technology-based companies, some of which may have a relationship with SVB. We are in communication with our largest Technology Platform partners and we are not aware of any impact on our business from private or public companies with potential exposure to SVB.

Cautionary Statement Regarding Forward-Looking Statements

Certain of the statements above are forward-looking and as such are not historical facts. These forward-looking statements are not guarantees of performance. Such statements can be identified by the fact that they do not relate strictly to historical or current facts. Words such as “we see”, “anticipate”, “believe”, “continue”, “could”, “expect”, “intend”, “may”, “future”, “strategy”, “might”, “plan”, “should”, “would”, “will be”, “will continue”, “will likely result” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Factors that could cause actual results to differ materially from those contemplated by these forward-looking statements include: (i) the effect of and uncertainties related to macroeconomic factors such as inflation, rising interest rates and any impact or deterioration in the banking industry and credit markets, including related to the closure of Silicon Valley Bank; (ii) our ability to achieve profitability and continued growth across our business in the future; (iii) the impact on our business of the regulatory environment and complexities with compliance related to such environment, including any further extension of the student loan payment moratorium or loan forgiveness, and our expectations regarding the return to pre-pandemic student loan demand levels; (iv) our ability to realize the benefits of being a bank holding company and operating SoFi Bank; (v) our ability to respond and adapt to changing market and economic conditions, including inflationary pressures and rising interest rates; (vi) our ability to continue to drive brand awareness and realize the benefits or our integrated multi-media marketing and advertising campaigns; (vii) our ability to vertically integrate our businesses and accelerate the pace of innovation of our financial products; (viii) our ability to manage our growth effectively and our expectations regarding the development and expansion of our business; (ix) our ability to access sources of capital on acceptable terms or at all, including debt financing and other sources of capital to finance operations and growth; (x) the success of our continued investments in our Financial Services segment and in our business generally; (xi) the success of our marketing efforts and our ability to expand our member base; (xii) our ability to maintain our leadership position in certain categories of our business and to grow market share in existing markets or any new markets we may enter; (xiii) our ability to develop new products, features and functionality that are competitive and meet market needs; (xiv) our ability to realize the benefits of our strategy, including what we refer to as our Financial Services Productivity Loop; (xv) our ability to make accurate credit and pricing decisions or effectively forecast our loss rates; (xvi) our ability to establish and maintain an effective system of internal controls over financial reporting; (xvii) our expectations with respect to our anticipated investment levels in our Technology Platform segment and our expected margins in that segment, including our ability to realize the benefits of the Technisys acquisition; and (xviii) the outcome of any legal or governmental proceedings that may be instituted against us. The foregoing list of factors is not exhaustive. You should carefully consider the foregoing factors and the other risks and uncertainties set forth in the section titled “Risk Factors” in our last annual report on Form 10-K, as filed with the Securities and Exchange Commission, and those that are included in any of our future filings with the Securities and Exchange Commission.

These forward-looking statements are based on information available as of the date hereof and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing our views as of any subsequent date, and we do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

As a result of a number of known and unknown risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking statements. You should not place undue reliance on these forward-looking statements.

Availability of Other Information About SoFi

Investors and others should note that we communicate with our investors and the public using our website (https://www.sofi.com), the investor relations website (https://investors.sofi.com), and on social media (Twitter and LinkedIn), including but not limited to investor presentations and investor fact sheets, Securities and Exchange Commission filings, press releases, public conference calls and webcasts. The information that SoFi posts on these channels and websites could be deemed to be material information. As a result, SoFi encourages investors, the media, and others interested in SoFi to review the information that is posted on these channels, including the investor relations website, on a regular basis. This list of channels may be updated from time to time on SoFi’s investor relations website and may include additional social media channels. The contents of SoFi’s website or these channels, or any other website that may be accessed from its website or these channels, shall not be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended.

[ad_2]