[ad_1]

The housing bears have ratcheted up their rhetoric lately, calling for an impeding crash.

It’s not a crazy notion with home prices clearly unaffordable and mortgage rates no longer anywhere near 3%.

But generally, a crash or bubble is preceded by creative financing of some sort.

Back in 2006, it was zero down mortgages, stated income loans, option ARMs, and other much worse things.

Today, the culprit is a higher-priced 30-year fixed mortgage, which isn’t all that creative.

Home Sellers Can’t Afford to Sell Right Now

The housing market is super weird at the moment. Even if homeowners want to sell, they often can’t.

Or have little desire to due to the strange mortgage rate environment.

In short, most existing owners have mortgage rates at or below 5%, per recent HMDA data. And most hold 30-year fixed-rate mortgages.

Some refer to these home loans as “golden handcuffs” because they trap homeowners, but also offer something of value.

The issue is these homeowners can’t move because you can’t take your mortgage with you (mortgage disruptors are you listening?).

Let’s consider a homeowner who purchased a property in 2018 for $500,000 and then refinanced in 2021 when the 30-year fixed was sub-3%.

We’ll pretend their property is now valued at $700,000, and their loan amount is just over $360,000.

Their monthly principal and interest payment is about $1,550. What a steal.

Now consider they’re looking to move up to a larger home to accommodate a growing family.

The asking price is $850,000 and the mortgage rate is 6.5%. If they put down 20%, a $680,000 loan amount at 6.5% costs nearly $4,300.

We’re talking a near-200% increase in mortgage payment. And this isn’t an uncommon scenario.

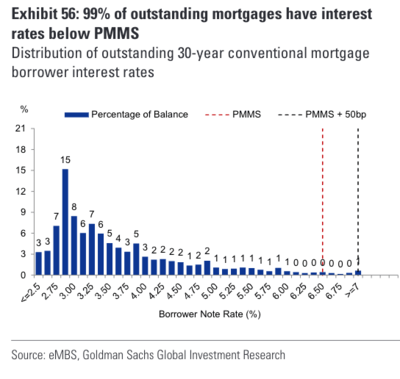

99% of Borrowers Now Hold Mortgage Rates Below Market Rates

A new chart has been circulating from Goldman Sachs that shows 99% of outstanding mortgages are priced below Freddie Mac’s weekly survey rate.

That survey rate was 6.65% at last glance, meaning virtually all existing homeowners have mortgage rates below that.

If you examine it closely, 28% of current owners have a rate below 3%, and another 44% have rates below 4%.

That’s 72% of current properties with a mortgage priced below 4%. You expect them to trade that for a 6.5% or even 7% mortgage rate?

For 99% of existing homeowners with a mortgage, there’s little incentive (or desire) to move from a mortgage financing standpoint.

Sure, some situations may warrant a move, and roughly 42% of homes in the U.S. are owned free and clear (no home loan attached).

But this paints a very different housing market than the one seen back in 2007.

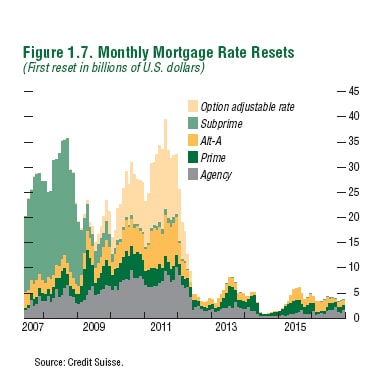

Homeowners Couldn’t Afford to Stay in 2007

Back during the Great Recession housing market, another chart was circulating, and it looked nothing like the current one. In fact, it was quite the opposite.

It displayed the hundreds of billions in adjustable-rate mortgages (ARMs) that were due to reset in coming months and years.

By reset, I mean adjust much higher, either to a fully-amortizing payment from negative amortization (or from interest-only).

Or those that were simply adjusting to the fully-indexed rate after the initial teaser rate was exhausted.

In either case, the payment was expected to rise substantially, likely leading to payment shock. And more importantly, an unaffordable mortgage.

And remember, many of these homeowners weren’t properly qualified for a mortgage to begin with.

Included in the chart were option ARMs, subprime loans, Alt-A mortgages, and standard prime and agency stuff.

The chart was terrifying and basically summed up the unsustainable housing market in one simple graph. In those days, homeowners couldn’t afford to stay.

So for those looking to draw parallels between now and then, you might want to review the two charts side by side.

Sure, home prices are inflated at the moment, and mortgage rates are pricey. But it’s just not the same housing market.

Yes, something has to give, but I don’t know if existing homeowners are going to be giving up their sub-4% mortgage rate.

What we need for a healthy housing market is long-term fixed mortgage rates back in the 4-5% range.

This would be helpful for new buyers, existing homeowners looking to move, and even the Fed!

[ad_2]