[ad_1]

Well, so much for mortgage rates falling just in time for the spring home buying season.

While many expected interest rates to be lower by now, they’ve proven to be pretty sticky at current levels.

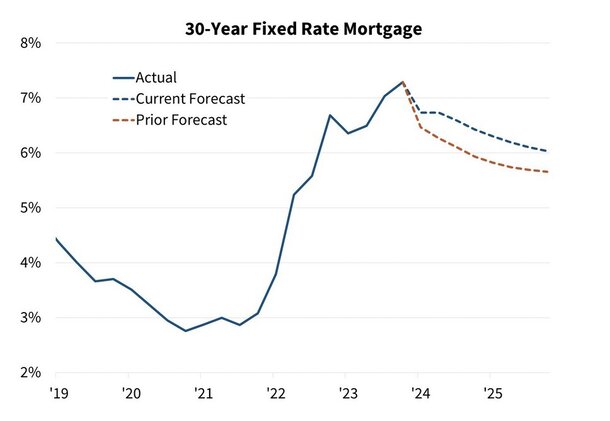

At last glance, the 30-year fixed is still hovering close to 7%, albeit better than October 2023 when it was around 8%.

But there was hope we’d see rates in the 6% range by now and maybe even lower if the Fed had cut rates earlier.

Instead, rates are actually pretty well aligned with the 2024 mortgage rate predictions made at the end of last year.

The likes of Fannie Mae and the Mortgage Bankers Association pegged the popular loan program at 7% for the first quarter of 2024. And that’s pretty much where we stand today.

The bad news is they’ve now indicated that it could take longer for rates to fall to more agreeable levels.

Fannie Mae Has Adjusted Its Mortgage Rate Forecast Higher for 2024 and 2025

In Fannie Mae’s March forecast, they noted that their “interest rate forecast has been upgraded.”

And not upgraded in a good way. Upgraded as in expect higher mortgage rates for the foreseeable future.

Just how bad is it? Well, after making adjustments a month earlier, they’ve since made upgrades of four-tenths and five-tenths, for the years 2024 and 2025, respectively.

This puts the 30-year fixed at an average of 6.6% in 2024 and 6.2% in 2025. In other words, no sub-6% mortgage rate for the next two years! Ouch!

In January, their forecast called for a 5.8% 30-year fixed in the fourth quarter of 2024, and a relatively low 5.5% by the end of 2025.

Freddie Mac Also Expects Mortgage Rates to Stay Above 6.5% in the First Half of 2024

Meanwhile, Freddie Mac released a new outlook that calls for mortgage rates to remain high through at least the first half of 2024.

They noted that 30-year mortgage rates will stay above 6.5% through the second quarter of 2024.

It’s unclear what happens after that, but there’s not a lot of optimism at the moment.

This should translate to lower mortgage volume, with rate and term refinance activity hard to come by.

And purchase activity also constrained by things like a continued lack of for-sale supply and mortgage rate lock-in.

However, they do expect home prices to increase by about 2.5% in 2024 and another 2.1% 2025.

Whether this keeps up with inflation is another story…

Why Aren’t Mortgage Rates Coming Down?

Simply put, the economy continues to run too hot. As a rule of thumb, good economic news leads to higher interest rates. And vice versa.

The reason is a strong economy typically results to inflation, which is bad for bond prices and mortgage-backed securities.

That price pressure requires higher yields, which translates to higher mortgage rates. So if you want lower rates, you kind of need to root for economic strife.

Due to this robust economy, the Federal Reserve has maintained its restrictive monetary policy.

While there were expectations of a series of rate cuts in 2024, including one as early as this March, the Fed balked today.

And there’s a chance rate cuts will remain elusive for the time being.

Ultimately, inflation continues to run high and unemployment remains low. Until that changes, the Fed won’t “pivot” and cut rates. They’ll simply stay the course.

While the Fed doesn’t directly control mortgage rates, their long-term policy decisions can dictate the direction of 10-year treasury yields and also 30-year mortgage rates.

Until economic conditions worsen, don’t expect the Fed to pivot and begin cutting its own federal funds rate.

Perhaps It’s Better to Say Mortgage Rates Will Be Elevated for Longer

There’s a popular phrase “higher for longer,” in reference to the Fed’s monetary policy needing to remain restrictive for a longer period of time to reach its goals.

When it comes to mortgage rates, perhaps it’s more accurate to say “elevated for longer.” That is to say they won’t necessarily go higher from their current levels.

But they may remain at these higher levels for longer than originally anticipated. So it’s not like we’ll necessarily see mortgage rates move up from here.

Or that they’ll go back to those scary 8% rates seen in October 2023. But they could linger in this unpleasant range throughout 2024. And maybe even into 2025.

This may make that date the rate, marry the house thing hard to achieve

If you recall when mortgage rates were super low, many forecasts called for higher rates year in and year out.

Yet each year, the forecasts proved to be incorrect as rates reached new all-time lows and stayed at/near those levels for much longer than expected.

Sadly, the same thing is possible now, just the other way around. So instead of rates doing what the forecasters expect, they’ll continue to remain sticky high.

The funny part is the economists will be wrong in both instances. Wrong about them rising for many years. And possibly wrong again about them falling back down to earth.

Go figure.

[ad_2]